Stock Options Trading Strategies: 10 That Actually Work

Options reward a defined plan and punish guessing. The strategies that actually work are those that are proven, are purpose-built, have a known risk/reward, and not far out of the money lottery tickets that pay off once and cost you the rest of the year.

If traders say a plan "works," it doesn't ensure a profit. It means that it has a known job, a known risk profile and a known market condition which it is aimed at.

This guide organizes 10 fundamental stock options trading strategies around what you want to accomplish: Make money, trade a trend, profit from a range, trade volatility, and hedge a position.

You get the payoff math, the perfect conditions, and an honest risk type, together with a framework for picking out between them.

First, the honesty that has to sit underneath all of it.

Options are high risk, leveraged and complex. Many options traders lose money. All of the strategies below can fail, even if used properly.

The content is intended for educational purposes only, and should not be taken as an investment or financial advice. Consider each example as an illustration; paper-trade before real money trading; don't trade an instrument you don't understand.

Options strategies 101: defined risk vs undefined risk

First let's discuss the components before the list.

A call option is an option that gives the buyer the right to buy a stock at a certain price. A put is an option to sell the stock at a specific price.

The strike price is the fixed price; the contract's expiry date is the expiry; and the price paid or received for the contract is the options premium.

Typically, each contract will cover 100 shares. If you sell an option and the buyer exercises the option, then you are assigned and you have to honor the trade.

There are two other forces that impact all options trades.

Implied volatility is the amount of volatility that the market expects, and it widens or narrows the price of options.

Time decay slowly erodes an option's value as expiry approaches. Time decay and volatility are the two factors that ultimately determine which strategies work for which conditions.

The line that separates all things from one another: defined risk versus undefined risk.

A defined risk strategy is one in which you know where the maximum loss will occur when you enter the trade. You can view the worst case prior to placing your buy.

An undefined-risk strategy is one that can have an unlimited or significant loss possibility, such as a large win with just one big move.

Defined-risk strategies | Undefined-risk strategies |

Covered call | Naked (uncovered) call |

Cash-secured put | Naked (uncovered) put |

Bull call and bear put spreads | Short straddle |

Credit spreads | Short strangle |

Iron condor and iron butterfly | |

Protective put and collar |

Recommendation: If just beginning to trade options, try using defined-risk strategies.

All of the items in the main list below are defined risk by design. The undefined-risk plays get their own clearly labeled caution section later.

The 10 best stock options trading strategies that actually work

There is no ‘one-size-fits-all' solution. It's all about your outlook on the market, the level of volatility you're experiencing and your tolerance for risk.

So the below list is organized by purpose and an honest risk profile is provided next to each. All strategies keep the same 6 fields to make comparison easy.

Income strategies

1. Covered call

Market view: Neutral to slightly bullish on a stock that you already hold in 100-share blocks. You are willing to sell at the strike (no strong bull market anticipation).

How it is built: Own 100 shares and sell one out-of-the-money call above the current price. You receive the option's premium in one lump sum.

Profit, loss, breakeven: Maximum profit is the premium received plus any profit from the stock up to the call strike. Max loss is a stock that approaches zero, but is protected by the premium. Breakeven is equal to your cost basis on the stock minus the premium.

Risk type: Defined on the option side, as the responsibility is backed by your stocks. The actual danger is the stock dropping. Upside above the strike is capped.

Trade-off: You limit your profit potential above the strike price, but you also get cash now. It is akin to a limit sell order, except that you get paid while you wait.

Payoff Shape: An increasing line that levels off at the strike price.

2. Cash-secured put

Market view: Neutral to bullish. You really want to purchase 100 shares at the strike and want income, or you want to get the stock at a discount.

How it is built: Sell one out-of-the-money put and set aside the cash to buy 100 shares at the strike if you are assigned. It's the cash backing that makes this a cash-secured put instead of a naked one.

Profit, loss, breakeven: Max profit equals the premium received. If the stock is down to zero, the max loss is quite large, depending on the strike, of course, and is calculated as (strike minus premium) times 100. Breakeven is the strike minus the premium.

Risk type: Defined, capped at the strike falling to zero. You may be assigned the shares.

Trade-off: You must be willing to own the shares and your profit is capped at the premium.

Payoff shape: A flat profit line at the premium that turns downward below the breakeven.

Directional strategies

3. Bull call spread (debit)

Market view: Moderately bullish. You'll expect an increase, but a modest one.

How it is built: Buy a lower-strike call and sell a higher-strike call with the same expiry, for a net debit. A bull call spread is one of the purest of the options spread strategies for a bullish trading perspective.

Profit, loss, breakeven: Max profit equals the spread width minus the net debit. The maximum loss is equal to the net debit paid. The breakeven is the long call strike plus the debit.

Risk type: Defined on both sides, and cheaper than buying a naked call.

Trade-off: Profit is limited to the short strike and the move must occur before expiry.

Payoff shape: Line that increases and then plateaus at the top strike.

4. Bear put spread (debit)

Market view: Moderately bearish. You expect a decline but not a collapse.

How it is built: Buy a higher-strike put and sell a lower-strike put with the same expiry, for a net debit.

Profit, loss, breakeven: The maximum profit is the spread width minus the net debit. The maximum loss is the net Debit paid. The breakeven is the long put strike minus the debit.

Risk type: Defined on both sides, and cheaper than buying a naked put.

Trade-off: Profit limited by lower strike.

Payoff shape: A declining line that flattens out below the bottom strike.

5. Bull put credit spread (credit)

Market view: Neutral to moderately bullish. The stock is expected to remain above a desired level.

How it is built: Sell a higher-strike put and buy a lower-strike put with the same expiry, for a net credit. This credit spread is one of the more popular options income strategies because its credit premium is received up front.

Profit, loss, breakeven: Max profit equals the net credit. The maximum loss is the width of the spread minus the credit. Breakeven equals the short put strike minus the credit.

Risk type: Defined with time decay on your side.

Trade-off: Accepting a lesser defined profit for a greater defined risk. It's a safer option than selling a naked put.

Payoff shape: A flat profit line at the credit that steps down to a fixed loss below the breakeven.

Range-bound and neutral strategies

6. Iron condor

Market view: Neutral. You are looking for the stock to remain range-bound through expiration and want to see a decrease in implied volatility.

How it is built: Sell an out-of-the-money bull put spread and an out-of-the-money bear call spread, four legs on the same expiry, for a net credit.

Example: stock at $100, sell the 95 put and buy the 90 put, sell the 105 call and buy the 110 call. That is a condor with $5 wings. A $2.00 credit gives a $200 max profit and a $300 max loss.

The iron condor is typically executed around 30-45 days to expiry.

Profit, loss, breakeven: Max profit equals the net credit. The maximum loss will be the wing width minus the credit. Two breakevens: the short put strike minus the credit, and the short call strike plus the credit.

Risk type: Defined. Time decay and volatility decline are to your benefit.

Trade-off: Low dollar profit relative to the risk, and four legs means four times the commissions. Position should be managed if price is approaching a short strike.

Payoff shape: A flat profit zone in the middle with a fixed loss on each side.

7. Iron butterfly

Market view: Neutral. You expect the stock to settle very near a specific price, the short strike, and volatility to fall.

How it is built: Sell an at-the-money call and an at-the-money put at the same strike, then buy a further out-of-the-money call and put for protection, four legs for a net credit. It is akin to an iron condor that has both short strikes at the same price.

Profit, loss, breakeven: Max profit equals the net credit, realized only if the stock closes at the short strike. Max loss equals the wing width minus the credit. Breakevens equal the short strike plus or minus the credit.

Risk type: Defined.

Trade-off: A wider premium compared to an iron condor and a smaller profit range. It requires a specific result.

Payoff shape: A steep tent at the short strike and drops to fixed payoffs on the wings.

Volatility strategies

8. Long straddle

Market view: You expect a big move but are unsure of direction, for example before earnings or another catalyst, and you expect volatility to rise.

How it is built: Buy a call and a put at the same at-the-money strike and expiry, for a net debit.

Profit, loss, breakeven: Max profit is large in either direction, theoretically unlimited to the upside. Max loss equals the total premium paid, if the stock pins the strike. Two breakevens: the strike plus the total premium, and the strike minus the total premium.

Risk type: Defined loss, the premium, but expensive. The price of the move has to be greater than the premiums combined.

Trade-off: You pay for both options, so the move has to be large. Time decay and a post-event drop in implied volatility (often called an IV crush after earnings) come at a cost to you. Many straddles lose to exactly that.

Payoff shape: A V-shape dipping to a fixed loss at the strike and climbing on both sides.

Hedging strategies

9. Protective put

Market view: Bullish and holding a stock, but you want downside insurance.

How it is built: Own 100 shares and buy one put on the same underlying. Premium is the cost. A protective put is a married put, paid for and held alongside your shares.

Profit, loss, breakeven: Max profit equals the stock's upside minus the premium. Max loss is floored at (stock cost minus put strike plus premium). Breakeven equals the stock cost plus the premium.

Risk type: Defined downside. The put is a kind of insurance.

Trade-off: The premium is a drag on returns, the cost of insurance, and if the stock rises the put expires worthless.

Payoff shape: A stock line that is rising and hard bottomed at the put strike.

10. Collar

Market view: Holding a stock and wanting downside protection at low or zero cost, and willing to cap upside in exchange.

How it is built: Own 100 shares, buy a protective put, and sell a covered call to finance the put. The net cost can be near zero.

Profit, loss, breakeven: Max profit is capped at the call strike minus the net cost. Max loss is floored at the put strike. Breakevens depend on the net cost.

Risk type: Defined on both sides.

Trade-off: You cap upside through the sold call in exchange for cheap or free downside protection through the put. It is a popular way to protect unrealized gains.

Payoff shape: A rising line bounded by a floor below and a ceiling above.

Master comparison table

Strategy | Market view | Risk type | Max profit | Max loss | Ideal conditions |

Covered call | Neutral to mildly bullish | Defined | Premium plus gain to strike | Stock toward zero, less premium | You own shares, expect calm or slow rise |

Cash-secured put | Neutral to bullish | Defined | Premium | Strike toward zero, less premium | Happy to own at a discount |

Bull call spread | Moderately bullish | Defined | Spread width less debit | Net debit | Measured upside before expiry |

Bear put spread | Moderately bearish | Defined | Spread width less debit | Net debit | Measured downside before expiry |

Bull put credit spread | Neutral to bullish | Defined | Net credit | Width less credit | Stock holds above a level, high IV |

Iron condor | Neutral, range-bound | Defined | Net credit | Wing width less credit | Range-bound, falling volatility |

Iron butterfly | Neutral, pinned | Defined | Net credit | Wing width less credit | Settles near a precise price |

Long straddle | Big move, unknown direction | Defined loss | Large either way | Total premium | Rising volatility, pre-catalyst |

Protective put | Bullish, wants insurance | Defined | Upside less premium | Floored at put strike | Holding stock, want a floor |

Collar | Holding, wants cheap protection | Defined | Capped at call strike | Floored at put strike | Protecting unrealized gains |

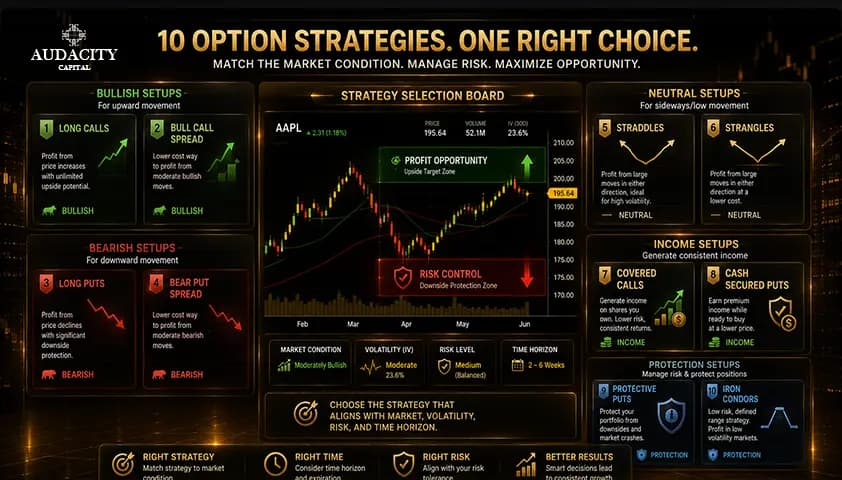

How to choose the right options strategy

There is no master strategy that fits every market. Choosing well means matching the tool to the conditions, and four questions do most of the work.

Q1: What is your market view?

Bullish, bearish, neutral and range-bound, or expecting a big move of unknown direction. Your directional read narrows the field immediately.

Q2: What is the volatility environment?

When implied volatility is high, premium-selling strategies like credit spreads and iron condors are often favored, because you are selling expensive premiums. When implied volatility is low, buying options through debit spreads or a straddle usually makes more sense, since premium is cheaper.

Q3: What is your risk tolerance?

Start with defined-risk strategies, where the worst case is visible up front. Only move beyond them when you fully understand the math.

Q4: What does your account allow?

Some strategies need margin and a higher broker approval tier. Selling naked options, in particular, requires a higher level than buying calls or defined-risk spreads.

Market view | Volatility | Strategy type to consider |

Bullish | Low IV | Bull call spread, long call |

Bullish | High IV | Bull put credit spread, cash-secured put |

Bearish | Low IV | Bear put spread |

Bearish | High IV | Bear call credit spread |

Neutral, range-bound | High IV | Iron condor, iron butterfly |

Big move, unknown direction | Low IV | Long straddle |

Higher-risk strategies to approach with caution

Some popular strategies are undefined-risk, and especially newer traders should avoid them. They sit outside the main 10 for a reason.

1. Naked (uncovered) call.

Selling a call without owning the stock. Risk is theoretically unlimited, because the stock can rise indefinitely while you are obligated to deliver. Defined-risk alternative: a bear call credit spread, which buys a higher call to cap the loss.

2. Naked (uncovered) put.

Selling a put without the cash set aside. Risk is substantial, since the stock can fall to zero. Defined-risk alternative: a cash-secured put, or a bull put credit spread that buys a lower put to cap the loss.

3. Short straddle.

Selling a call and a put at the same strike. Risk is unlimited on the upside and substantial on the downside, so a single large move on either side can be punishing. Defined-risk alternative: an iron butterfly.

4. Short strangle.

Selling an out-of-the-money call and put. Same unlimited or substantial exposure on both sides. Defined-risk alternative: an iron condor.

These strategies require high approval levels and significant margin, and one large move can cause an outsized loss. For almost every view above, a defined-risk version exists, and for most traders it is the better choice.

Common options trading mistakes to avoid

Most losses are not bad luck. They trace back to a handful of avoidable errors, and each one ties straight back to the risk-first theme.

Mistake 1: Trading without understanding assignment and expiration.

If you sell options, you can be assigned. Know what happens at expiry before you open the position.

Mistake 2: Ignoring implied volatility.

Buying options into high IV before earnings often ends in an IV crush, where the option loses value even when you guessed direction correctly.

Mistake 3: Over-leveraging.

Options are leveraged, so position sizing matters more, not less. One outsized trade can undo months of progress.

Mistake 4: Ignoring commissions and fees.

Multi-leg trades multiply costs, and condors and butterflies with four legs feel that the most.

Mistake 5: Holding to expiration.

Letting positions run into the final hours exposes you to pin risk and unwanted assignment. Many traders manage and close early on purpose.

Mistake 6: Chasing cheap far-out-of-the-money options.

The lottery-ticket trade is cheap because it rarely pays. Treating it as a strategy is the fastest way to bleed an account.

FAQ

Defined-risk income strategies such as covered calls and cash-secured puts, along with defined-risk spreads, are the usual starting points. The maximum loss is known up front, which makes them easier to manage while you learn. Even so, every one of them can lose, so paper-trade first.

Some strategies are built for income, but none guarantee it. Results depend on market conditions, and every strategy can lose, so treat income strategies as a risk-managed approach rather than a salary. Position sizing and discipline matter far more than any single trade.

A defined-risk strategy has a known maximum loss the moment you open it, which you can see before you trade. An undefined-risk strategy, such as a naked option or a short straddle, carries theoretically unlimited or substantial loss. Beginners should stay on the defined-risk side.

Buying options and many defined-risk spreads need only options approval, not a margin account. Selling naked options and some spreads require a margin account and a higher approval level. Your broker decides which tiers unlock which strategies.

When implied volatility is elevated, premium is expensive, so premium-selling defined-risk strategies like credit spreads and iron condors are often favored. When volatility is low, buying options or using debit spreads tends to make more sense. Always check the volatility environment before choosing the structure.

It varies by strategy and broker. Covered calls and cash-secured puts require enough capital to hold or buy 100 shares, while defined-risk spreads can need far less, plus whatever margin the broker requires. Start small and scale only as your understanding grows.

Assignment means you are obligated to buy or sell the underlying stock at the strike. Understanding assignment, and managing positions before expiry, is part of trading any strategy that involves selling options. Surprise assignments are usually a sign the position was left unmanaged too long.

Single long options are simple but lose value to time decay and need a large move to pay off. Defined-risk strategies let you express a view with a known maximum loss and often a higher probability of profit, at the cost of capped gains. The trade-off is structure and discipline in exchange for control.

Готовы применить дисциплинированный риск к криптовалютам? Изучите новые криптоинструменты Audacity Capital и примените свою торговую стратегию.

Узнать большеРассылка

Подпишитесь на нашу рассылку.

Присоединяйтесь к нашему сообществу

Начните свое путешествие сегодня с нашей бесплатной пробной версией

С гордостью демонстрируйте свои навыки и достижения с помощью сертификатов и получайте признание за свой тяжелый труд и преданность делу от потенциальных инвесторов и коллег.

Бесплатная пробная версия