Best Local Payment Methods for Forex Prop Trading

You pass the challenge. You build a profit. Then comes the moment that turns every promise into reality: you click "request payout" and wait to see if the money actually lands in your country, in your currency, without eating half of it in fees.

The best local payment methods for forex prop trading are the ones offered by a firm that reliably pays, that moves money fastest and cheapest into your country, and that fit your withdrawal size and record-keeping needs.

For most traders worldwide, that means crypto or stablecoins like USDT for speed and low fees, or a local bank transfer or Wise route for larger amounts and cleaner records.

But the reframe underneath all of this matters more than any single rail. The payment method is table stakes. Whether the firm actually pays you, on time and without excuses, is the thing that decides everything.

The Two Sides of Prop Firm Payments: Funding vs Withdrawing

There are two completely different payment events in prop trading, and traders often optimize for the wrong one.

The Deposit: Paying Your Challenge Fee

This is the one-time fee you pay to start an Ability Challenge, an Ability One evaluation, or an instant-funding program.

You usually pay by card or crypto, and sometimes by local methods. It is a small, one-off transaction. Speed and convenience matter, but not much else.

The Payout: Withdrawing Your Profit Split

This is the recurring, high-stakes side. It is how you receive your share of profits for as long as you trade with the firm. This is where fees, delays, and reliability compound over time.

Here is the point most traders miss. You pay a fee once, but you withdraw for as long as you trade.

So optimize for the payout, not the deposit. The two sides often use different rails: card or crypto going in, and bank transfer, Wise, or crypto coming out. When you compare prop firm payment methods, judge the firm on how it pays you, not on how easily it takes your money.

How Prop Firms Actually Move Money

Most prop firms do not pay you from a company bank account. That surprises a lot of new traders.

Instead, firms route payouts through third-party contractor-payment platforms like Deel, Rise, and Plane, or through crypto rails such as USDT and USDC on-chain, or a mix of both. That is why, shortly after you get funded, you often receive a separate onboarding invite from Deel or Rise, and why setup happens before your first payout, not during it.

Why do firms work this way?

- These platforms handle cross-border compliance and KYC verification for payouts across 150+ countries, which a single company bank account cannot do at scale.

- They deliver money in local currency, so you are not always stuck converting US dollars yourself.

- They manage tax paperwork and reporting that varies wildly from country to country.

The practical takeaway: the firm decides which rails it offers, and you pick from that menu. Availability varies by country, so what works for a trader in London may not be an option for a trader in Lagos. We are not endorsing any processor here. We are just explaining the machinery so you know what to expect.

Best Local Payment Methods for Forex Prop Trading, Compared

This is the core of the guide. Below, every common method follows the same block: what it is, speed, typical fees, who and where it suits, and what to watch out for.

All figures are ranges. Fees and timelines vary by firm and country, so treat everything as "typical," never as a guarantee.

Group A: Fastest and Most Global

1. Crypto and Stablecoins (USDT, USDC)

What it is: On-chain transfer of stablecoins, with USDT the most common and USDC growing, or less often BTC and ETH. USDT on TRC-20 (Tron) is the most widely supported and cheapest rail. ERC-20 (Ethereum) costs more. Stablecoins are pegged near 1:1 to the US dollar, so there is no price swing between requesting and receiving.

Speed: The fastest option. Often minutes to a few hours after approval.

Typical fees: A minimal network fee, from cents to a few dollars on TRC-20. Usually no processor cut.

Best for: Traders anywhere, especially in India, Africa, Latin America, and Southeast Asia, and anyone in a country where cards or wires are slow or restricted. Ideal for smaller, more frequent withdrawals.

Watch-outs: You need a wallet and must send it to the exact correct network and address, because errors are irreversible.

Choose a stablecoin, not BTC or ETH, to avoid volatility. Local crypto rules vary, and you still owe tax on the value received. Some firms do not offer crypto at all.

When people talk about USDT / stablecoin prop firm payouts, this is the rail they mean, and it is why crypto prop firm withdrawals have become the default for so much of the world.

Group B: Fintech and Contractor-Payment Rails

2. Wise

What it is: A multi-currency transfer service covering 40+ currencies at the mid-market rate. The firm, directly or through Deel or Rise, sends money to your Wise balance or your local bank.

Speed: Often same-day to 1 to 3 business days.

Typical fees: Low and transparent, a small percentage plus the mid-market FX rate. Cheaper than banks or PayPal.

Best for: UK and European traders, anyone who wants a clean bank-style record without heavy wire fees, and multi-currency earners.

Watch-outs: Country support varies, and the name on the Wise account must match your KYC. For many traders, using Wise for prop firm payouts is the sweet spot between speed and clean documentation.

3. Rise

What it is: A contractor-payment platform some firms use. It pays out via bank transfer, crypto, or debit card. You receive a Rise onboarding link after you get funded.

Speed: Fast once set up. The crypto option can be near-instant, while bank transfers are slower.

Typical fees: Vary depending on the method you choose inside Rise.

Best for: Traders at firms that use Rise, and anyone who wants to pick bank or crypto in one place.

Watch-outs: Set up your Rise profile and complete KYC in the first week. Do not wait until you need the money. Rise payments are only fast if your account is already verified.

4. Deel (and Plane)

What it is: Global payroll and contractor platforms operating across 150+ countries. They handle local bank transfer, crypto, and sometimes PayPal, plus the tax and compliance paperwork. Plane is a similar international-payout platform some firms use for local-currency bank transfers.

Speed: ACH or crypto can be roughly 24 hours. International bank transfers run roughly 3 to 7 business days.

Typical fees: Generally absorbed by the firm, though FX or withdrawal fees may apply on your side.

Best for: International traders who need local-currency delivery and documented payments.

Watch-outs: Expect a separate onboarding email, and check your spam folder for it. Payments may be reported to your tax authority as part of the platform's compliance. Because Deel prop firm payments involve formal reporting, they leave a clean paper trail that suits larger, documented withdrawals.

5. E-wallets (Skrill, Neteller, PayPal)

What it is: Digital wallets some firms use for payouts and deposits. Familiar and quick to receive.

Speed: Fast, often same-day.

Typical fees: Can be higher. PayPal and Skrill conversion and withdrawal fees run roughly 1.9% to 3.5%.

Best for: Traders who already use these wallets and value speed over lowest cost, and regions where these wallets are common.

Watch-outs: Conversion fees eat into your take-home amount. Availability and limits vary by country, and not every firm supports them. Skrill and Neteller e-wallets are convenient, but do the math on fees before you choose them for larger sums.

Group C: Traditional Bank Rails

6. Local Bank Transfer

What it is: A payout sent to your domestic bank account in local currency, usually through a processor's local rails such as Deel, Plane, or Wise, rather than an international wire.

Speed: Often 1 to 3 business days domestically.

Typical fees: Low to moderate. There is no large international-wire charge when it runs on a local rail.

Best for: Traders in countries with fast local clearing, such as UK Faster Payments, EU SEPA, India IMPS and UPI-linked transfers, and US ACH. Good for larger amounts and for money going straight into an existing bank.

Watch-outs: Availability depends on whether the firm's processor supports your country. Slower than crypto.

7. International Wire (SWIFT) and ACH

What it is: A traditional cross-border wire, or a US domestic ACH transfer. This is the fallback when faster rails are not available.

Speed: A bank wire (SWIFT) transfer runs roughly 2 to 5 business days, sometimes up to 7. ACH runs roughly 1 to 3.

Typical fees: SWIFT flat fees run roughly $15 to $50, and are sometimes charged at both ends.

Best for: Large withdrawals where security and a clear paper trail matter, US traders using ACH, and situations where no other option exists.

Watch-outs: The slowest and priciest choice for small amounts. Intermediary-bank fees can surprise you.

8. Cards (Visa / Mastercard), Mainly the Deposit Side

What it is: The most common way to pay a challenge fee. Some firms also push payouts to cards via Visa Direct or Mastercard Send.

Speed: Instant for deposits. Card payouts, where offered, usually take 1 to 2 days.

Typical fees: Low for deposits. Card-payout fees vary.

Best for: Funding a challenge quickly. Payouts only where the firm offers a card-push option.

Watch-outs: Cards are a deposit tool first. Do not assume you can withdraw to one. A chargeback on a challenge fee can get you banned.

Best Local Payment Method by Region

Availability is everything here. The same rail that dominates in one country may not even exist in another. Below are the go-to local options by region, why they work, and one watch-out for each.

*Verify against your specific firm and country before you rely on any of them. None of this is tax or financial advice.

India

Go-to: UPI and IMPS-linked local bank transfer for small-to-mid amounts, plus USDT for speed and to sidestep FX friction. Many India-based traders are paid via crypto or a Wise or Deel local transfer. The UPI (India) local transfer route is fast and familiar for domestic sums.

Why: Fast domestic rails handle smaller amounts well, and crypto covers borderless speed when bank routing is slow.

Watch-out: Crypto is taxed in India and the rules keep evolving, so verify the current position and speak to a professional. Remember this is simulated prop trading, not retail FX with an Indian broker.

UK and Europe

Go-to: Wise or a local bank transfer, using UK Faster Payments or a SEPA (Europe) transfer, for clean records, plus USDT if you want speed.

Why: Strong, cheap banking rails make bank or Wise an excellent default here.

Watch-out: Name-match on KYC is essential, and reserve SWIFT for non-SEPA edge cases.

United States

Go-to: ACH or a domestic wire, or crypto such as USDT and USDC for speed. Rise and Deel are common here.

Why: ACH is cheap and reliable domestically, and crypto gets you paid in hours.

Watch-out: Payments are likely reported, for example on Form 1099-NEC over $600. Keep records, and remember tax applies on receipt. US residents may only participate where permitted, typically via DXTrade.

UAE and MENA

Go-to: Local bank transfer in AED or USDT. Crypto is widely used for cross-border speed.

Why: Local transfer suits larger sums, and crypto handles fast cross-border movement.

Watch-out: Confirm the firm's processor supports the UAE, and verify local crypto rules.

Africa (Nigeria, Kenya, South Africa and others)

Go-to: USDT is often the most practical option. M-Pesa works where supported, and a local bank via a processor otherwise.

Why: International banking can be limited or slow, so borderless crypto often wins.

Watch-out: Take care with wallets and networks, and verify firm support country by country.

Latin America (Brazil, Mexico and others)

Go-to: USDT for speed, plus PIX in Brazil and other local rails via processors where offered.

Why: PIX is near-instant in Brazil, and crypto covers the rest quickly.

Watch-out: Local-currency volatility can affect what you keep, so verify support for your country.

Southeast Asia (Philippines, Indonesia, Vietnam and others)

Go-to: Local bank transfer via processors plus USDT. Crypto is common where banking is friction-heavy.

Why: Local rails offer familiarity, and crypto adds speed and reach.

Watch-out: Availability varies widely from one country to the next.

Payment Methods Compared at a Glance

Method | Typical speed | Typical fees | Best for | Main watch-out |

Crypto / stablecoins (USDT) | Minutes to hours | Network fee only | Anywhere; restricted-banking regions; small or frequent | Wallet and network errors; use a stablecoin |

Wise | Same-day to 3 days | Low, mid-market FX | UK and EU; clean records; multi-currency | Country support; name must match KYC |

Rise | Fast once set up | Varies by method | Firms that use Rise; bank-or-crypto choice | Set up and complete KYC in week one |

Deel / Plane | ~24h to 7 days | Usually firm-absorbed | International; local-currency delivery | Separate onboarding email; may be tax-reported |

E-wallets (Skrill / Neteller / PayPal) | Often same-day | ~1.9% to 3.5% | Existing wallet users; speed over cost | Conversion fees; limited availability |

Local bank transfer | 1 to 3 days | Low to moderate | Fast-clearing countries; larger amounts | Depends on processor support |

Wire (SWIFT) / ACH | SWIFT 2 to 5 days; ACH 1 to 3 | SWIFT ~$15 to $50 | Large sums; paper trail; US (ACH) | Slow and pricey for small amounts |

Cards (deposit side) | Instant deposit | Low for deposits | Funding a challenge fast | Rarely a payout method; no chargebacks |

How to Choose the Right Method for Your Situation

Work through these questions in order, and the right method usually reveals itself.

1. Which methods does your firm actually offer?

Start here. There is no point choosing a rail your firm does not support.

2. How fast do you need it?

Crypto lands in hours. Bank transfer and Wise take days.

3. How large is the withdrawal?

Small and frequent points you toward crypto or an e-wallet. Large points you toward a bank or wire for the record.

4. How important are clean records for tax?

Bank transfer and Wise leave the cleanest trail.

5. What is normal and legal in your country?

This one is non-negotiable, and it varies.

Rule of thumb: default to crypto or USDT for speed and low fees if you are comfortable with a wallet.

Use Wise or a local bank for larger amounts and cleaner records. This is not financial or tax advice, and your situation varies.

The Part That Matters More Than the Method: Does the Firm Actually Pay?

Here is the uncomfortable truth. The best payment method on earth is worthless if the firm stalls, moves the goalposts, or refuses to pay. The payout is the exact moment a firm's promises stop being marketing and become real.

Ground yourself in the numbers. Across a large industry dataset of roughly 300,000 accounts analyzed by Finance Magnates and FPFX Tech, only about 14% of traders passed their challenge, and only around 7% ever reached a payout.

Read that again.

Most challenges never reach a payout, and no payment rail changes that. A funded account is a test of skill under structure, not a shortcut to income.

So before you pay any fee, learn to read the firm, not just the rail.

Red-flag models to avoid.

These are behaviors, not names.

- Vague or unbounded processing windows with no committed timeline.

- "Manual review" that clearly cannot scale as trader numbers grow.

- Hidden minimum thresholds that surface only when you try to withdraw.

- Sudden rule changes that appear right before a payout is due.

- Payments to a third-party or different-name account rejected without a clear reason.

Green flags to look for.

- Documented payouts with proof and consistent, on-time cycles.

- Automated processing rather than case-by-case delays.

- Clear rails and timelines published up front, before you buy.

- Active, credible trader-community reports of getting paid.

When you understand how to withdraw money from a prop firm in practice, you realize the method is the last 10% of the problem. The first 90% is choosing a firm with a genuine payout track record. Verify that before you spend a cent.

Before You Pay a Challenge Fee: The Payment Questions to Ask

Ten minutes of due diligence prevents most post-purchase regret. Run through this checklist first.

- Which payout rails and currencies does the firm support for my specific country?

- Which crypto chains and tokens does it use, for example TRC-20 or USDC?

- Is the challenge fee refunded on the first payout, fully or partly, and under what conditions?

- What is the minimum withdrawal threshold?

- What is the payout cycle, on-demand versus bi-weekly or monthly, and what is the stated processing time?

- What KYC is required, and must the payout account match your name?

Understand the firm's prop firm payout methods and its rules for your country before you buy is the single cheapest form of insurance in this business.

Getting Paid Without Delays

Most payout delays are avoidable and self-inflicted. These steps keep your money moving.

1. Complete KYC early and accurately: Have your ID and proof of address ready and correct. Clean KYC verification for payouts is what unlocks fast withdrawals later.

2. Set up your Deel, Rise, Wise, or crypto profile in the first week of funding: Do not wait until you need the money.

3. Make sure the payout account is in your own name and matches your KYC: Third-party and joint accounts are rejected as fraud prevention.

4. Close all positions before requesting: Most firms require you to be flat.

5. Confirm you have met the minimum threshold before you request.

6. Save every confirmation and screenshot for your records.

Trade With a Firm That Pays on Time

If reliable, on-time payouts are what you are really looking for, that is exactly the standard Audacity Capital was built on. Founded in London in 2012, with a 14-year trading legacy, activity in 140+ countries, and over $210M paid out to traders, the firm's whole pitch rests on transparency and paying skilled traders what they have earned.

Audacity Capital is a forex and CFD prop firm running on MetaTrader 5 and DXTrade, with three funded routes to suit different traders: the Ability Challenge (a two-step evaluation), Ability One (a one-step evaluation), and the FTP, or Funded Trader Program, with instant funding.

Payouts run on a bi-weekly cycle from 14 days after your first trade, with up to 90% profit share on the challenge route. No consistency rule, news trading allowed, weekend holding allowed, EAs allowed, and copy trading allowed.

If you want to demonstrate your skill first, the free monthly trading competition is a low-pressure way to start. Explore the Funded Trader Program or join the monthly competition when you are ready.

FAQ

Usually the firm absorbs the processor fee, but you may still pay a network fee on crypto, or an FX or withdrawal fee on your side. Check the firm's payout page before you request, because it varies by rail and by firm.

Usually yes. Many traders pay by card or crypto and then withdraw via bank, Wise, or crypto. Confirm both the deposit and the payout menus for your country before you buy.

Stablecoins remove the price swings you get with BTC or ETH, so the main risks are wallet or network errors and rare de-peg events. Send on the correct network, TRC-20 or ERC-20, to the exact address, and it is usually the fastest option available.

Crypto, usually USDT, is the common fallback because it is borderless. Verify the firm actually offers a crypto payout before you rely on it.

Those platforms handle cross-border compliance, identity checks, local-currency delivery, and tax paperwork across 150+ countries, which a firm's own bank account cannot do at scale. That is also why you receive a separate onboarding invite.

Often yes, through a processor's local rails or a Wise transfer. Otherwise you receive US dollars or USDT and convert it yourself, which adds a small cost.

The first one is slower because of KYC. After setup, crypto typically lands in hours, and bank or Wise takes one to three business days, though the cycle, on-demand versus scheduled, depends on the firm.

¿Listo para aplicar un riesgo disciplinado a las criptomonedas? Explore los nuevos instrumentos de cripto de Audacity Capital y traiga su estrategia de trading.

Aprender másBoletín

Únase a nuestro boletín para mantenerse al día.

Únete a Nuestra Comunidad Social

Comienza Tu Viaje Hoy Con Nuestra Prueba Gratuita

Muestra con orgullo tus habilidades y logros a través de certificados y obtén reconocimiento por tu arduo trabajo y dedicación de posibles inversores y compañeros.

Prueba GratuitaArtículos Relacionados

Topstep vs Apex: Which Prop Firm Is Better?( Honest Comparison & Review in 2026)

Compare Topstep vs Apex Trader Funding in 2026. Review fees, drawdown rules, profit splits, news trading, payouts, and account options to find the best prop firm.

Can You Hold Trades Overnight or Over the Weekend on a Prop Firm?

Can you hold trades overnight or over the weekend on a prop firm? Learn the rules, risks, gap exposure, and which prop firms allow swing trading.

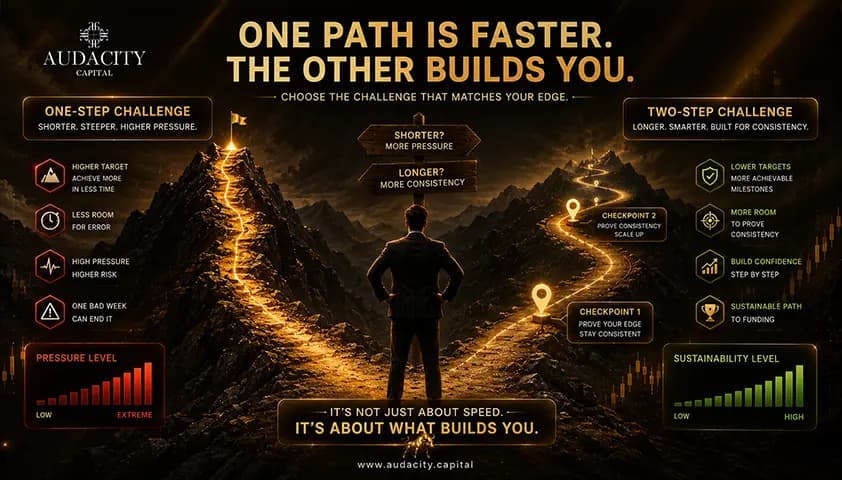

One-Step vs Two-Step Prop Firm Challenges: Which Model Actually Fits You

An honest, balanced breakdown of the one step vs two step prop firm decision: speed, targets, drawdown, cost, pass rates, and a choose-by-profile framework.

Do You Pay Taxes on Prop Firm Payouts? A Funded Trader's Guide

In almost every country, prop firm payouts are taxable income, not capital gains. Learn how they are taxed, what you can deduct, and why records matter.